Best Factors for Establishing a Singapore Holding Company

Discover the Engaging Topics in This Article

Understanding a Singapore-Based Holding Company

What Is an Operating Company?

The World’s Top Businesses Choose Holding Structures

- The Virgin Group

- The Trump Organization

- Apple Inc.

Holding Company Quick Facts

- Holding companies can adopt various organizational structures, such as limited liability companies, limited partnerships, trusts, or foundations. The limited liability company is the most prevalent form of holding company structure.

- Although holding companies frequently exert significant influence over their subsidiaries through their involvement in (or control of) the subsidiary’s board, they usually do not manage the subsidiary’s daily operations.

- A key advantage of a Singapore holding company structure is the insulation it provides from the subsidiary’s liabilities, thereby offering loss protection.

- The parent company can consolidate and allocate the resources of its subsidiaries. Consequently, the parent benefits from a subsidiary’s success without being negatively impacted beyond its original investment if the subsidiary underperforms.

Singapore Holding Company Examples

Johnson & Johnson

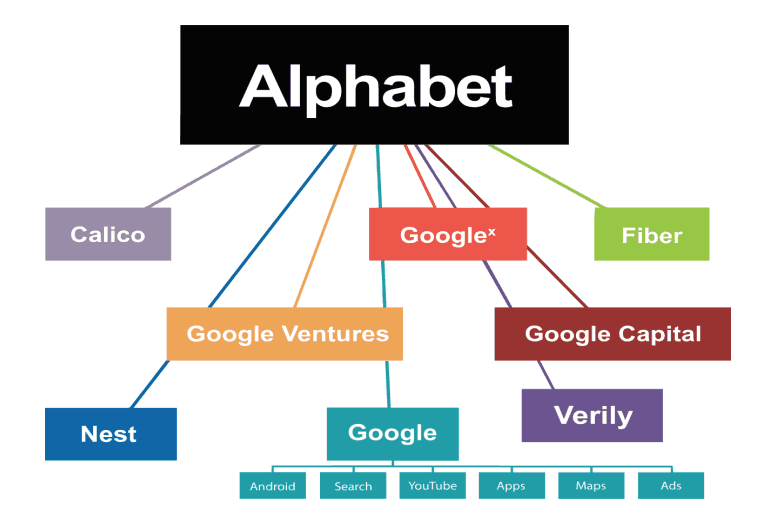

Alphabet

Alphabet is mostly a collection of companies. The largest of which, of course, is Google. This newer Google is a bit slimmed down, with the companies that are pretty far afield of our main internet products contained in Alphabet instead... Fundamentally, we believe this allows us more management scale, as we can run things independently that aren't very related.

Berkshire Hathaway - a Quintessential Holding Company

Today, Berkshire Hathaway doesn’t operate any textile mills. Rather, it’s a holding company that owns hundreds of subsidiaries and holds stock in many other public and private companies. Its holding portfolio changes day by day as assets are acquired and sold.

To get a sense of the scale of its holdings, click and expand the above figure (from finbox.io). They include assets in industries as diverse as railroads, auto insurance, finance, and men’s apparel. In fact, it’s hard to find a sector where Berkshire Hathaway does not have assets.

Bershire Hathaway’s holding include:

- Banking (Wells Fargo)

- Business jet rentals (NetJets)

- Candy (See’s Candies)

- Fast food (Dairy Queen)

- Furniture (RC Willey Home Furnishings, CORT)

- Insurance (GEICO)

- Jewelry (Borsheim’s Fine Jewelry, Helzberg Diamonds, Ben Bridge Jeweler, Inc.)

- Modular houses (Clayton Homes)

- Newspapers (The Buffalo News)

- Trucking (McLane Co., Inc.)

Historically, the company has made its acquisitions using reserves from its insurance subsidiaries, also known as the “float”. These are the funds paid to an insurance company as premiums that have not yet been paid to cover claims. Berkshire Hathaway has insurance reserves of over $100 billion.

Buffet is an ardent follower of Benjamin Graham and is the classic value investor. He purchases companies that are fundamentally robust but are facing hard times and are therefore available cheap. Buffet cleans up his acquisitions, often by replacing management so they start generating dividends. The dividends are used to fund future acquisitions.

Buffet is laser focused on dividends. He usually doesn’t acquire companies that don’t pay dividends. Nearly all of his large holdings (e.g., Apple, Coca-Cola, American Express, etc.) have robust track records of paying dividends. Buffet’s basic mantra is: Acquire companies with fundamentals that are strong enough to allow regular cash payments to shareholders without soldely chasingrevenue growth. Watch the video below to understand Berkshire Hathaway’s basic business model.

Unlock the Advantages of a Singapore Holding Company: Discover the Essential Benefits Today

Loss Insulation

Holding companies are insulated from the losses of their subsidiaries, so a holding company isn’t liable for acts of a subsidiary if the parent didn’t actively participate in and have control over the actions of the subsidiary. However, there are exceptions for fraud and negligence).

Singapore’s legal and tax regulatory framework provides full support for such loss insulation. Therefore, if a subsidiary company declares bankruptcy, its creditors cannot legally pursue the holding company. Thus, a Singapore holding company offers a very good loss insulation strategy. With such a structure, lines of business that have unique risk profiles can be segregated into a separate subsidiary.

For example, a fast food restaurant chain may own one subsidiary that owns the know-how patents, a second that owns real estate assets, a third that owns brand assets, and other subsidiaries that own and operate individual franchises. If there’s a fire in one of the franchise restaurants that injures customers, the brand and other assets of the business are protected from liability.

Additionally, if you set up the individual companies within your Singapore holding company correctly, the any debt liability of one subsidiary won’t affect the other holding companies or the parent company.

Tax-Efficient Holding Company Structures

A Singapore holding company framework can contribute to reducing the total tax liability of the business if individual subsidiaries are strategically established to create a tax-efficient holding company structure. Tax-efficient holding company structures can enhance tax-saving strategies by:

-

- Utilizing double tax avoidance agreements (DTAAs) (such as the India-Singapore DTAA or the Malaysia-Singapore DTA) in multiple jurisdictions

- Minimizing or postponing the personal taxes of company owners

Evading capital gain taxes - Bypassing taxes on dividends, interest, and royalties

- Capitalizing on tax incentives by aligning subsidiary objectives with incentives

- Employing retained earnings across subsidiaries in a tax-effective manner

Each subsidiary files its tax returns individually, and these returns are consolidated at the parent company level. A well-designed tax-efficient holding company structure can lower the overall tax liability of the holding company by strategically placing each subsidiary in a jurisdiction that offers the most significant tax advantages for its line of business.

Additionally, losses from one entity can be utilized to counterbalance profits from another. The group may also employ intra-group financing techniques. For example, a company can lend the retained earnings of a profit-generating subsidiary to another subsidiary experiencing growth to attain more favorable tax results. In this aspect, Singapore is a particularly advantageous jurisdiction.

List of Tax Benefits Available in Singapore for Holding Companies

Singapore employs a single-tier or full-imputation tax system, resulting in corporate profits being taxed only once. As a result, Singapore does not impose taxes on dividends from a subsidiary to its Singapore parent company, and there is no withholding tax when dividends are distributed to either residents or non-residents. Similarly, interest paid by a subsidiary to the parent is not subject to withholding tax and is considered a pre-tax expense. However, royalties and specific technical service fees paid to foreign corporations may be subject to a 10% and 17% tax, respectively, if no exemption applies and the tax rate is not reduced under a tax treaty. Nevertheless, careful structuring of corporate entities can help optimize these taxes.

Dividends obtained from a holding company's foreign subsidiaries might be exempt from corporate tax, provided the 'subject to tax' and 'foreign headline tax rate' conditions are satisfied. Essentially, these conditions mandate that the subsidiary's profits should, in theory, be taxed at a minimum of 15% in the subsidiary's country of domicile. There is no requirement for an actual payment to the subsidiary's country of domicile due to exemptions or incentives. As a result, dividends from tax-neutral or low-tax jurisdictions might be subject to tax in Singapore when distributed to the parent company. Presently, Singapore does not have controlled foreign company regulations, so the undistributed income of foreign subsidiaries might not be taxable. These provisions can be utilized to create an international corporate holding structure that can significantly reduce—or even completely eliminate—the structure's total tax burden.

Additionally, Singapore does not impose any capital gains tax, nor is there a transfer tax on share sales. Consequently, the sale of assets or subsidiaries by the parent company is not considered a taxable event at either the subsidiary or holding company level. However, if capital gains make up the majority of a company's income and the holding period of the sold asset is relatively short, they might be treated as ordinary income and subject to income tax. It is worth noting that since capital gains are not taxed, capital losses are typically non-tax deductible.

Singapore provides various tax incentives for intellectual property (IP) holdings. The IP Development Incentive (IDI) program offers concessionary tax rates of 5% or 10% on qualifying royalty and other IP income until 2023, provided certain levels of expenditure, job creation, and other economic commitments are met within Singapore. Additionally, you may be eligible for deductions on qualifying expenses incurred for research and development activities, IP registration, and licensing.

Typically, foreign-owned holding companies are considered non-residents. To achieve tax resident status, the company must apply to the Inland Revenue Authority of Singapore (IRAS) and obtain a Certificate of Residence (COR), which might be required by foreign tax authorities to claim tax treaty benefits. It is important to note that a foreign jurisdiction may deny access to tax reliefs even if a COR is presented. When issuing a COR, the IRAS considers a combination of factors, including:

- Whether control and management are exercised in Singapore (e.g., are board of directors meetings held in Singapore?)

- The validity of reasons for establishing a holding company in Singapore

- If the company receives administrative services from a Singaporean company

- The presence of related entities conducting business in Singapore

- The employment of an executive director (not a nominee) and a C-level employee based in Singapore

Concerning intra-group transactions, Singapore law mandates adherence to the "arm's length principle." This principle dictates that prices for transactions between related parties should be equivalent to those that unrelated parties would charge in similar situations. Companies with a gross revenue exceeding SGD 10 million may be required to submit transfer pricing documentation for transactions with related parties above specific thresholds, if requested by the IRAS. More information on Singapore Transfer Pricing regulations can be found in our guide.

Ultimate Parent Entities (UPEs) in Singapore, which are part of large multinational corporations with a consolidated group revenue of SGD 1.125 billion or more, are required to file a country-by-country report. This report should include crucial details about revenue, taxes paid and accrued, employment, capital, retained earnings, tangible assets, and business activities for both the parent company and its subsidiaries. These regulations make Singapore a secure and favorable location for establishing your tax-efficient holding company. However, it is essential to carefully design the holding structure to avoid being perceived as a tax avoidance scheme. The structure must have an economic rationale and commercial reasons to justify its existence; otherwise, anti-avoidance regulations related to transfer pricing, thin capitalization, and interest deductibility limitations may apply. Inter-company transactions should be conducted at arm's length and appropriately documented and reported. For professional assistance in designing a tax-optimized Singapore holding company structure that meets Singapore compliance requirements, feel free to contact us. A reliable corporate services partner can help you create a corporate structure tailored for tax optimization while ensuring it remains compliant with Singapore's regulations.

Holding companies in Singapore have no restrictions on the location of assets they own. The subsidiaries under a Singapore holding company can be situated in Singapore or any other foreign country, offering exceptional versatility for this type of structure.

Singapore provides unique government incentives, including the Finance & Treasury Centre (FTC) Incentive, Global Trader Programme, and Pioneer Certificate Incentive & Development and Expansion Incentive, specifically for certain Singapore holding companies. These incentives are commonly known as Headquarter Incentives.

Singapore holding companies benefit from advantageous accounting practices for consolidated financial statements, allowing losses from one subsidiary to counterbalance gains from another. Moreover, a favorable accounting system is in place for passive income earned by a Singapore holding company. Furthermore, specific regulations, like the Financial Holding Companies Act, typically streamline the compliance process for holding companies in Singapore.

A Singapore holding company can safeguard valuable assets like patents, trademarks, and intellectual property by placing them under the ownership of a distinct subsidiary. This arrangement not only defends the assets against unwarranted legal challenges but also facilitates smooth buying and selling of patent portfolios. When a holding company is owned by a high-net-worth individual, their personal assets receive protection, as they are technically owned by the corporation and not the person. This separation effectively shields the individual from debt liabilities, lawsuits, and other potential risks.

Organizing assets within individual subsidiaries streamlines transactions involving those assets. By selling a subsidiary as an independent unit, there is no need for extensive restructuring or complex accounting reviews and audits to establish its value, as the accounts are already managed separately. This approach significantly simplifies the acquisition and disposal of assets when they are held within distinct subsidiaries.

A parent company can play a crucial role in succession planning, offering tax deferral benefits while ensuring a seamless transfer of the entire estate to the next generation. Singapore's regulatory environment is especially conducive to trust structures that incorporate holding companies. Utilizing a holding company for intergenerational wealth transfers provides the following advantages:

- Establishment and consistent enforcement of clear governance rules for family wealth

- Simplified transfer of diverse assets located in multiple countries as a single entity

- Streamlined risk management, asset protection, and wealth preservation through a single point of delegation to professional managers

- Development of a comprehensive intergenerational strategy that combines asset holdings with other tools, such as wills, family offices, foundations, jurisdiction selection for residence, and lasting power of attorney

A Singapore holding company structure effectively separates the failure probabilities of individual subsidiaries, significantly reducing the likelihood of a systemic failure within the entire business. This lowers the overall business risk and consequently reduces its cost of capital. The holding company can secure better financing terms than it would under a single company structure.

Additionally, holding companies can offer downstream guarantees for subsidiaries, enabling improved financing terms for subsidiary projects and lowering their cost of capital. A Singapore holding company structure can be designed to segregate capital-intensive subsidiaries (which may carry substantial debt) from operating subsidiaries. In case an indebted subsidiary fails, its issues do not affect other parts of the overall business, which can continue functioning. Financial institutions recognize this advantage and reward it with a lower cost of capital for the entire business.

Typically, business owners exercise control over the holding and subsidiary companies via the board of directors. This arrangement enables the business to centralize strategic coordination across the subsidiaries while still allowing them the flexibility to operate autonomously. A holding company structure can also help maintain consistent ownership and governance policies throughout the subsidiaries. For instance, new investors in a business might require that all patents and IP assets be owned by a single subsidiary to ensure transparent management. This approach facilitates the implementation of standardized governance practices and safeguards the investors' interests while streamlining the coordination of various subsidiaries within the holding company structure.

By shielding owners from the daily operations of a subsidiary, a holding company structure can help maintain confidentiality or discretion regarding their involvement or strategic plans. This separation can be beneficial in protecting the owners' privacy and keeping sensitive business strategies or investment decisions confidential, making it an attractive option for those seeking to maintain a low profile while managing their business interests.

Holding Company Challenges

Holding company managers are often pulled in multiple directions by the demands of their subsidiaries. They may have to make crucial decisions about a subsidiary without in-depth knowledge about its immediate business activities. This lack of information can result in sub-optimal decisions.

Conversely, subsidiary managers may not have enough information about the overall strategy or goals of the parent company. The interests of the two companies and its managers may not be correctly aligned. For instance, a subsidiary may wish to buy raw material from the best supplier in the market, but the parent company may want it to buy it from one of its subsidiaries. Such competing interests across management teams can result in conflict and poor business decisions.

The holding company structure provides the opportunity to create opaque business relationships. Such a framework becomes a disadvantage for the minority shareholders who might not have an accurate picture of the whole business. Majority owners can use transfer pricing or preferred supplier relationships to their advantage. This can be a particularly serious issue if ownership of the holding company and all subsidiaries is not symmetric and parties own different proportions of the subsidiaries.

Because the market doesn’t have a clear picture of the operations of all subsidiaries, it may penalize a holding company's stock price. Furthermore, if the holding company owns subsidiaries that are not performing well financially, the market may penalize the holding company disproportionately for the performance of the subsidiary while not giving the parent full credit for the financial performance of the parent company.

How to Set Up a Singapore Holding Company

If you do decide to move forward with establishing a holding company, your objectives will dictate the right type and structure for it.

Types of Holding Companies

There are only two types of holding companies in Singapore: investment and financial. Each has its own particular registration criteria, but there’s not much difference in terms of taxation:

- An investment holding company is the default structure for companies operating outside the finance, banking, and insurance industries;

- A financial holding company is meant for owning subsidiaries operating in the finance, banking, and insurance industry.

Types of Corporate Structures

How a Holding Company Structure Works

Investing Through the Holding Company

How Profits Flow

Intercompany Loans

Tax savings

Utilizing a Singapore-incorporated holding company for structuring investments can yield substantial tax benefits. Let’s consider a Japanese entrepreneur investing in Japan under two distinct scenarios:

Scenario 1: The Japanese entrepreneur directly invests in Japanese Company A

Scenario 2: The Japanese entrepreneur channels investments in Japanese Company A through Singapore holding Company B

| Scenario 1 (S$) | Scenario 2 (S$) | |

|---|---|---|

|

Corporate taxable income amount |

100 000 000 |

100 000 000 |

|

Corporate income tax rate (23.2%) |

23 200 000 |

23 200 000 |

|

Distributable surplus |

76 800 000 |

76 800 000 |

|

Withholding tax on distributed dividends (20.42% for individual shareholders and 5% for Singapore corporate shareholders under the Singapore-Japan DTA) |

15 682 000 |

3 840 000 |

|

Surplus |

61 118 000 |

72 960 000 |

|

Tax on dividend income (0% for individual shareholder and 0% for Singapore corporate shareholder under the Foreign Sourced Income Exemption) |

0 |

0 |

|

Net amount in the hands of shareholders |

61 118 000 |

72 960 000 |

Discover Why a Singapore Holding Company Could Be

Your Ultimate Solution

Objectively evaluate your goals by pinpointing which of the following outcomes you aim to achieve through a Singapore holding company structure:

- Separation of various business lines from subsidiary risks

- Tax efficiency

- Asset safeguarding

- Preparing for future asset transactions

- Intergenerational transfers

- Decreasing capital costs

- Consolidation and standardization of corporate control across business lines

- Privacy

If the above goals are not relevant to your business, a holding company may not suit your needs. However, if some of these aspects are crucial, contact CorporateServices.com to discuss your primary objectives and devise a beneficial and compliant structure to address them.

The types of assets that comprise your business will influence your decision. If your business has assets from more than one of the following categories or has only one type of asset spread across multiple jurisdictions, a holding company structure may be suitable for your situation.

- Equity Holdings: If your business owns minority (or full) stakes in other companies, those stakes can be held by individual subsidiaries.

- Active Businesses: If your business operates individual lines of business that can logically be separated into stand-alone entities, then each business should operate under a separate subsidiary.

- IP Assets: If your business owns intellectual property assets, these are excellent candidates for placement in one or more separate subsidiaries.

- Leasing: If parts of your business involve real estate or expensive equipment, those assets can be placed in separate subsidiaries and leased to other parts of the business.

- Financing: This is a complex topic, but essentially, if some parts of your business generate income while others are still growing, you should protect the income-generating parts in a separate subsidiary to shield them from the risks associated with the growing business that may be subject to greater risk.

Holding companies, as primarily financial structures, can be easily moved and restructured in response to changing tax environments without relocating underlying physical assets like plants and equipment.

A holding company's basic arrangement allows it to accumulate profits from subsidiaries for reinvestment or distribution to shareholders. It may also sell assets at times. Various stages in this process involve potential tax payments, including:

- Corporate and dividend tax at the subsidiary level

- Corporate tax at the holding company level

- Withholding tax when distributed to shareholders

- Personal income tax at shareholder level

- Capital gains if any subsidiary is sold

The goal of a well-designed structure is to eliminate or reduce most of these taxes. This can be achieved through strategies such as:

- Intercompany transfer payments for products or services

- Intercompany loans and interest payments

- Consolidation of tax returns at the holding company level

- Specialization of subsidiaries to utilize tax incentives

- Locating subsidiaries or holding companies in jurisdictions with no taxes on dividends and/or capital gains

- Optimizing for exit taxes

- Utilizing tax treaties

- Tax residence of the ultimate beneficial owners (UBO)

- Compliance with controlled foreign company (CFC) rules by optimizing ownership percentages

- IP licensing across subsidiaries

Moreover, some jurisdictions employ the "full imputation system," where profits are taxed only once at the level of the operating company generating them. Such jurisdictions are beneficial for holding company structures, with Singapore being an example.

Importantly, your structure should possess economic and commercial justification (or substance) that can be transparently reviewed by tax authorities. Without economic substance, your structure may face scrutiny and challenges. Some ways to meet substance tests include:

- Hiring local directors in the jurisdiction

- Establishing a local office for key documents and accounting records

- Hiring a local secretary in the jurisdiction

- Opening a local bank account

- Conducting annual general meetings to pass "mind and management" tests

Ensuring adequate R&D expenditure for IP assets

Given the above reasons, it's crucial to engage a corporate services firm experienced in these structures. The firm will assess your situation and advise whether a suitable structure can be designed to benefit your specific case. To learn more, explore incorporating a limited liability company in Singapore.

Another factor to consider is access to secure, efficient, and comprehensive financial services. It's crucial to establish a holding company structure only if these services can be offered to both parent and subsidiaries cost-effectively. Not every jurisdiction provides such services. However, Singapore delivers world-class financial services, with almost all major international banks having a presence there. Sophisticated capital market products and services are readily available in Singapore, including brokerage services, investment products, financial engineering services, M&A services, and art holding services, among others.

It's important to assess the added expense of establishing and managing multiple entities within a holding company structure against the advantages it provides. Singapore, once again, presents cost-effective solutions for creating and maintaining such a structure.

Ultimately, it's crucial to carefully select the jurisdiction in which you intend to establish your holding company and some or all of your subsidiaries. Additionally, it's essential to choose a corporate services firm that has in-depth knowledge of the jurisdiction's laws and can guide you throughout the process. Singapore is widely acknowledged as an outstanding jurisdiction for setting up holding companies due to the numerous benefits provided by its regulatory framework, tax system, and legal structure. To learn more, get in touch with CorporateServices.com today.

Conclusion

If you’re considering a holding company structure, Singapore is an excellent jurisdiction due to its favorable regulatory framework, tax policies, and legal system.

Choose a reputable corporate services partner in Singapore to ensure that your holding company structure meets the economic substance requirements and won’t encounter objections from regulatory authorities.

Setting up a Singapore holding company can be done online within a few days with the assistance of a reliable service provider. All you need to do is provide the necessary information and required documents. Your service provider will handle the filing and submission process on your behalf.

How Can We Help?

Are you in search of company incorporation, immigration, accounting, tax filing, or compliance services in Singapore? If so, CorporateServices.com is here to assist.

With our extensive experience in establishing holding companies, we can help you create the ideal structure for your business and asset holdings. You’ll receive a personalized solution designed to meet your specific needs, offering protection, privacy, risk mitigation, tax optimization, and operational efficiency. Please reach out to us if you need help registering a company in Singapore or if you’d like to transfer the administration of your existing company to our team.

Our Accreditations

Address

- 171, Tras Street #05-173A, Union Building Singapore 079025

- 51, Goldhill Plaza, #21-11/12, Singapore 308900

Phone Number

- (+65) 83822739

E-mail address

- info@moriiassociates.com